Michigan Car Accident Lawyers

Find out how our team of experienced Michigan auto and car accident attorneys can get you the compensation you deserve.

Choosing A Michigan Car Accident Lawyer

Anyone who has survived a car accident knows how upsetting the experience can be, especially if you or a loved one is seriously hurt. It only takes seconds for a crash to occur, yet the consequences can last a lifetime. And, unfortunately, insurance companies often pressure victims to make hasty decisions that affect their physical, emotional and financial well-being for years to come. That’s why hiring a Michigan car accident lawyer can help navigate this complicated situation.

Recovering the benefits and compensation you deserve is a lengthy and often-complicated procedure. And, understandably, most people are not thinking clearly in the aftermath of a major accident. A knowledgeable accident attorney helps you navigate the complex legal process so you can focus on recovering from your injuries. In addition, studies show victims who are represented by qualified car accident lawyers achieve far better financial outcomes than individuals who represent themselves.

Why People Choose Us To Be Their Michigan Car Accident Lawyers

We are Michigan’s most experienced personal injury law firm. Our skilled car accident attorneys have more than 800 years of combined experience winning high verdicts and settlements for our clients. Starting from our first conversation, we treat our clients like family. Whenever you need us, we are here to answer your questions and guide you through the complicated legal process required to win your case. We don’t stop fighting until you receive the compensation you deserve.

Reasons That Victims Of Car Accidents Hire Our Car Accident Lawyers:

- A car accident is a traumatic experience. Most people are not thinking clearly after a serious car crash. Therefore, you may be more likely to accept a hasty and often low-ball insurance settlement

- The insurance company is not on your side. This can be true of your own insurance company as well as the other driver’s. Your lawyer will be on your side from day one, fighting to make sure you receive the maximum amount possible.

- Michigan No-Fault law is extremely complicated. The Michigan No-Fault system was always confusing, and the recent reforms have made it even more so. Knowledgeable car accident lawyers understand the law and how the new changes may affect your case.

- It takes a skilled lawyer to win “pain and suffering” damages. In addition to medical benefits, seriously injured victims are often entitled to considerable compensation for intangible damages such as pain and suffering. However, plaintiffs must meet the new standards for “threshold injuries” in addition to proving the other party was at fault. A skilled lawyer will help you recover the maximum amount of compensation.

- You will achieve a better financial result when you hire an accident lawyer. Studies show that plaintiffs who are represented by experienced car accident lawyers receive larger verdicts and settlements than those who represent themselves.

280,000

CAR & TRUCK ACCIDENTS

OCCUR IN MI EACH YEAR

71,000

INJURIES YIELDED ANNUALLY

FROM THESE ACCIDENTS

Hiring A Michigan Car Accident Lawyer

As a rule, it’s wise to consult a lawyer after a vehicle accident, especially if you or anyone else is injured. The Michigan No-Fault system is complex, and the process for obtaining the benefits you are entitled to can be confusing for those unfamiliar with it.

What Our Car Accident Lawyers Will Do For You:

Our auto accident attorneys will explain your legal rights and advise you on the best way to obtain the benefits and compensation you are entitled to. We’ll file all the necessary paperwork, obtain relevant records and documents, interview witnesses and perform a multitude of other services.

Our experienced accident attorneys will also represent you in court if your case proceeds to trial. Most importantly, a lawyer will protect you from being taken advantage of by the insurance companies or at-fault driver(s). When you have a good lawyer on your side, your case is far more likely to succeed.

Additionally, an experienced Michigan car accident lawyer will evaluate your injuries to determine if you qualify for pain and suffering damages. In those cases, plaintiffs must meet the legal standard for a “threshold injury,” which requires extensive medical documentation. You will have a much better chance of success with a knowledgeable accident attorney on your side.

Areas We Serve

Additionally, an experienced Michigan car accident lawyer will evaluate your injuries to determine if you qualify for pain and suffering damages. In those cases, plaintiffs must meet the legal standard for a “threshold injury,” which requires extensive medical documentation. You will have a much better chance of success with a knowledgeable accident attorney on your side.

Free Consultations

Our experienced lawyers offer free no-obligation consultations to anyone who has been involved in a car accident. If you or a loved one was hurt in a crash, call us today. We will fight for your rights and help you win the benefits you and your family are entitled to. That’s The Bernstein Advantage®

Frequently Asked Questions About Car Accident Cases

How Does The New Michigan No-fault Law Impact My Car Accident Case?

If you are injured in an accident, your own insurance policy covers your medical expenses and related costs, even if you were at fault. These are considered first-party benefits, which include Personal Injury Protection (PIP) and Property Protection Insurance (PPI).

Michigan No-Fault law underwent sweeping reforms in 2019, many of which took effect July 1, 2020. Prior to that date, every Michigan No-Fault policy included unlimited lifetime medical benefits, including rehabilitation and home care. However, after July 1, 2020 policyholder can choose from a variety of Personal Injury Protection (PIP) medical benefit levels. Vehicle owners can keep their previous unlimited lifetime medical benefits, choose a lesser amount ($500,000, $250,000 or $50,000 for Medicaid recipients), or opt out of PIP medical coverage if they have Medicare or other qualified health coverage.

Other PIP benefits, which did not change under the new law, cover up to 85% of lost wages and $20/day for replacement services (such as housework and lawn care) for up to three years.

Because these cases involve complex legal issues, you need a No-Fault lawyer with extensive experience and a thorough knowledge of Michigan’s car crash related laws. In addition to a winning track record, we have the necessary expertise and resources to win the settlement you deserve. Contact us today to schedule your free consultation.

If you’d like to learn more, visit the following link to view and download our Michigan No-Fault Law resources.

Additional Michigan No-Fault Law Articles:

- The New No Fault Law and Medicare

- Does the New Michigan No Fault Law Cover Out-of-State Drivers

- The Six New Personal Injury Protection (PIP) Options

Should I Contact A Car Accident Lawyer If No One Was Injured In The Accident?

Even if there are no apparent injuries, you should still contact an accident attorney. Some conditions, such as soft tissue injuries, don’t always show up immediately. Or, an injury that appears minor right after the accident may worsen. This is true for you and your passengers as well as the occupants of the other vehicle(s) involved in the crash.

You want to avoid being blindsided if the other driver suddenly files a lawsuit against you.

Consulting a lawyer soon after your accident gives you and your legal team a head start should your case become more complicated.

Should I Hire A Car Accident Attorney For A Minor Accident?

Yes, it’s a good idea to contact a lawyer even if the accident appears minor. As discussed in the above section, seemingly minor injuries can worsen in the weeks or months following a crash. An accident lawyer will tell you what to expect in the event your condition (or another person’s) becomes more serious.

What Are The First Steps I Should Take After A Car Accident?

What you do immediately after an accident can affect what happens in the future. If you inadvertently admit fault or sign insurance papers prematurely, you may lose valuable insurance benefits as well as monetary compensation.

To protect your rights after being involved in a crash, here are some things you should do (and some you should avoid doing):

- Call for an ambulance if you or anyone else is hurt

- Move your car to the side of the road to wait for the police

- Take photos of the accident scene and all the vehicles involved

- Call an experienced car accident lawyer as soon as possible

- Exchange information with the other driver(s)

- Get contact information for all passengers and other witnesses

- Don’t admit fault or talk about the accident or your injuries with the other driver(s)

- Do not talk to an insurance adjuster or sign any papers before you speak to a lawyer

When Should I Call A Lawyer After An Accident?

We recommend calling a car accident lawyer as soon as possible after an accident occurs. The sooner you call, the sooner your legal team can begin working on your case. Starting right away is a good idea for several reasons:

- The clock starts ticking immediately on Michigan’s strict statutes of limitations and filing deadlines

- Witnesses’ memories are freshest right after an accident

- Evidence may disappear if too much time goes by

- Gathering necessary medical records and other documentation can be a lengthy process

- Your lawyer needs sufficient time to build a winning case

Additional Resources: Do You Need A Lawyer For a Car Accident That Was Not Your Fault?

Am I Entitled To Damages For Pain And Suffering After A Car Accident?

If you are seriously injured, and you were less than 50% at fault for the accident, you may be entitled to certain non-economic damages. These damages are intended to compensate victims for intangible losses such as pain and suffering and loss of companionship or consortium. Non-economic damages are also known as third-party benefits because they are typically paid by the insurance company of the at-fault driver.

Furthermore, victims must prove they have sustained a “threshold injury” to receive pain and suffering damages. This is defined as “…death, serious impairment of body function, or permanent serious disfigurement.”

However, it is common for insurers to claim the victim’s condition does not meet the legal standard. This is why you need an experienced car accident lawyer to gather the medical documentation and expert witness testimony necessary to build a winning case.

You may also be able to file a lawsuit to recoup excess economic losses such as medical expenses that exceed the driver’s Personal Injury Protection (PIP) medical coverage limit. Plaintiffs do not have to meet the threshold requirement to collect these third-party damages.

This applies to Michigan residents; out-of-state residents must meet the threshold requirement for both economic and non-economic damages.

How Much Is The Average Settlement For A Car Accident Case?

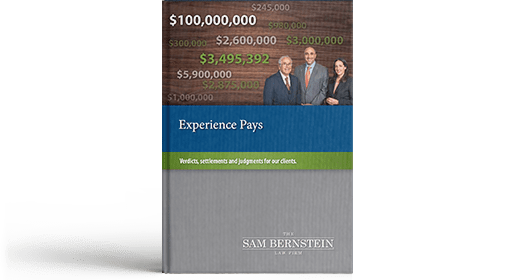

Over the past five decades, we have helped our clients recover more than $3.5 billion in verdicts and settlements. Whatever your circumstances, our team of experienced accident lawyers will fight to win the compensation you deserve.

While every case is different, the amount you receive depends on several factors. The severity of the injuries and the degree of negligence exhibited by the at-fault driver are major elements. For example, if a victim is seriously hurt because a driver was drunk or texting on a cell phone, the settlement is likely to be higher.

Settlements can range from $50,000 to millions of dollars. Our legal team won $5,900,000 for a client who suffered head injuries and multiple fractures after being rear-ended by a careless driver. We have helped other clients receive settlements of more than $2,500,000 for injuries caused by negligent motorists.

In addition, settlements are impacted by the amount of liability insurance the at-fault driver has. Under the new No-Fault law that took effect July 1, 2020, the minimum required liability limits were raised from $20,000 per person and $40,000 per accident to $50,000/$100,000.

Continued Reading: Understanding Car Accident Settlements

How Much Do Car Accident Lawyers Charge?

A reputable accident lawyer typically does not charge up-front fees or retainers to take your case. Personal injury attorneys, which includes car accident lawyers, work on a contingency basis.

This means they don’t collect their fee (typically one-third of the verdict or settlement) until your case is resolved. In addition, most accident lawyers charge for out-of-pocket expenses such as obtaining and copying medical records. However, in most cases, plaintiffs do not have to pay these costs until they receive their settlement.

Continued Reading: Car Accident Lawyer Fees

Statute Of Limitations: How Long After An Accident Can I Bring A Claim?

Michigan has a strict statute of limitations for filing claims or lawsuits following an accident. If you fail to meet the prescribed deadlines, you may lose your right to receive the compensation you are entitled to.

In general, accident victims have one year from the date of the accident to file a claim for Personal Injury Protection (PIP) benefits. This includes reimbursement for expenses such as medical bills, attendant care, mileage, lost wages and replacement services. Medical and related expenses are limited to the amount of PIP medical benefits selected by the policyholder. Lost wages and replacement services are covered for up to three years.

Moreover, victims have three years from the date of an accident to file a claim for non-economic damages such as pain and suffering. This timeline also applies to lawsuits filed to recoup excess economic losses such as medical expenses that exceed the driver’s Personal Injury Protection (PIP) medical coverage limit. These third-party benefits, which can be substantial, are typically paid by the insurer of the driver that caused the accident. In Michigan, victims are entitled to these damages only if they were less than 50% at fault for the accident.

What If I’m Hit By A Drunk Driver?

If you are injured by a drunk (or drugged) driver, you may have several legal options available, depending on the situation.

In addition to the Personal Injury Protection (PIP) benefits provided by the victim’s No-Fault policy, a severely injured plaintiff may be entitled to non-economic damages such as pain and suffering. The plaintiff may also be able to claim excess economic loss damages. These include medical expenses or lost wages that exceed the amounts covered by the victim’s No-Fault Personal Injury Protection (PIP) benefits.

To recover these damages, which are often substantial, the victim must file suit against the insurance company of the at-fault driver.

Insurance companies typically try to dispute these claims to avoid paying out large settlements to seriously injured victims. To win your case, you will have to provide extensive documentation and fill out numerous forms. This is where the expertise and resources of a skilled car accident attorney prove invaluable.

Finally, a victim may have grounds for a “dramshop” claim. This is the legal term for a lawsuit against a liquor store, bar, or other business, which illegally sold alcohol to the person whose unlawful behavior caused an accident. Under Michigan law, it is illegal to sell alcohol to a minor (under age 21) or to an adult who is visibly intoxicated.

Dramshop claims must be filed within 120 days after the victim retains an attorney.

For all of the above reasons, it’s crucial to contact us immediately if your accident involved a drunk driver.

Noteworthy Wins

We have championed the cause of car accident victims for three generations in Michigan. Our team of knowledgeable trial lawyers knows how to get the compensation you and your family deserve.

Hear from our Clients...

Trusted by thousands of satisfied Michigan clients and their families.

Recommended Reading

TAKING A MEMORIAL DAY ROAD TRIP? HOW TO AVOID A CAR ACCIDENT ON THIS DANGEROUS DRIVING WEEKEND

May 21, 2025

Read more

“OPERATION GHOST RIDER” TARGETS DISTRACTED DRIVERS IN MICHIGAN

May 12, 2025

NEW MICHIGAN CAR SEAT LAWS

April 2, 2025

SAFE DRIVING TIPS FOR MEMORIAL DAY WEEKEND

May 24, 2024

APRIL IS DISTRACTED DRIVING MONTH: WHAT TO KNOW ABOUT THIS DEADLY EPIDEMIC

April 30, 2024

ARE GOLF CARTS “STREET LEGAL” ON MICHIGAN ROADS?

April 9, 2024

DOES MICHIGAN NO-FAULT INSURANCE COVER NON-RESIDENT DRIVERS INVOLVED IN A CAR ACCIDENT?

April 9, 2024

MANY DRIVERS ARE UNAWARE IT’S ILLEGAL TO USE A HAND-HELD CELL PHONE: WHAT EVERY MICHIGAN MOTORIST SHOULD KNOW ABOUT THE NEW DISTRACTED DRIVING LAW

February 29, 2024

MICHIGAN’S SEAT BELT CRISIS: LINGERING PANDEMIC HABITS PUT MOTORISTS AT RISK

February 28, 2024

NEW ELECTRONIC SIGNS ON I-94 RECOMMEND SAFE SPEED LIMITS FOR WINTER DRIVERS

January 30, 2024

MICHIGAN SUPREME COURT ALLOWS FULL MEDICAL BENEFITS FOR VICTIMS INJURED BEFORE NO-FAULT REFORMS

January 30, 2024

WINTER CAR ACCIDENTS: NAVIGATING ICE AND SNOW AND RECEIVING THE COMPENSATION YOU DESERVE

January 30, 2024

WHAT MICHIGAN DRIVERS SHOULD KNOW ABOUT THE DEADLIEST NIGHT OF THE YEAR

November 22, 2023

LEAVES, RAIN AND ROADS: AVOIDING AUTUMN CAR ACCIDENTS

October 27, 2023

WHO IS RESPONSIBLE FOR A MICHIGAN CAR ACCIDENT INVOLVING AN ANIMAL?

October 27, 2023

IS IT IMPORTANT TO OBTAIN A POLICE REPORT AFTER A MICHIGAN CAR ACCIDENT?

October 3, 2023

THE DANGERS OF DRIVING WITH DEMENTIA

October 3, 2023

MICHIGAN LAWMAKERS APPROVE AUTOMATED SPEEDING TICKETS IN CONSTRUCTION ZONES

October 3, 2023

THE LATEST MICHIGAN CAR ACCIDENT STATISTICS: WHAT DRIVERS SHOULD KNOW

August 23, 2023

DANGEROUS DRIVING HABITS CAUSE SURGE IN FATAL MICHIGAN CAR ACCIDENTS

August 22, 2023

We are proud to be an official partner of the Detroit Lions®. We share common values including a commitment to hard work and grit in service to our clients and the community.

Contact us today!

No upfront fees. No risk. No pressure.

Put our three generations of experience to work for you. Don't wait to get the help you need! As Michigan's most experienced personal injury law firm, we've helped thousands of people just like you get the compensation they deserve. Your consultation is always free, and, with our No Fee Guarantee®, you won't pay anything until we win your case.

"*" indicates required fields